Contents

If you’re a company director, you may have heard of a holding company and the protection that it offers to your business structure. Most people set up a holding company to reduce tax and risks while their company grows, but it’s important to note that a holding company can still be liable for any debts incurred by its subsidiary companies.

This all depends on the situation, and there are a number of questions to ask before deciding whether the holding company is liable. But before we discuss these circumstances, it’s important to go through some key terms.

What Is A Holding Company?

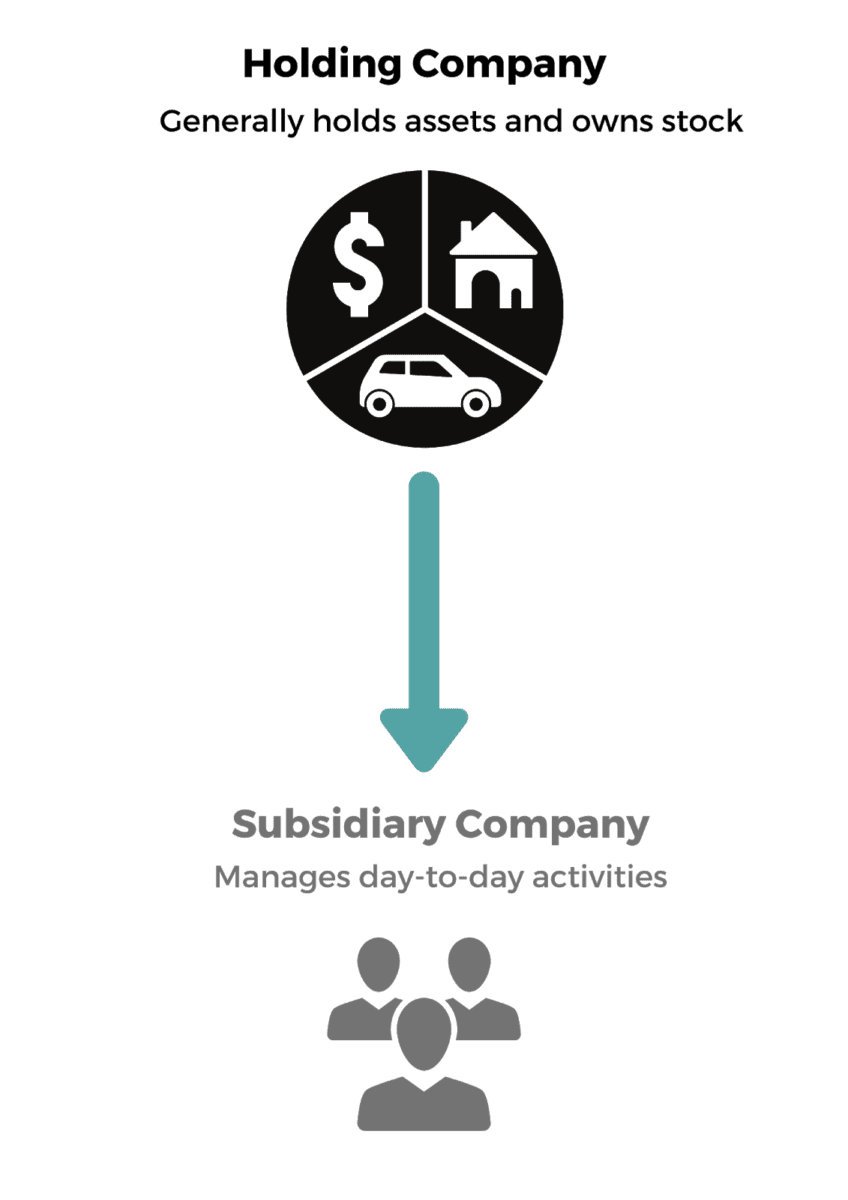

A holding company is usually set up to own shares or stock in its subsidiary companies, but is generally uninvolved in day-to-day activities like manufacturing or selling. It’s a good way to reduce the risks of a growing business structure because it protects your company assets.

For example, if a customer wanted to sue your company, they could only sue the subsidiary company that they had a legal relationship with. This means that all the company’s assets that are owned (or being ‘held’) by the holding company are protected.

What Is A Subsidiary Company?

A subsidiary company is the company that is owned by a parent or holding company. Following on from the example above, the subsidiary company would be the one exposed to the most risk of being sued. This is why a holding company is used as a safeguard, and generally owns most of the company assets.

This kind of company structure is also known as a dual company structure.

Here’s a diagram to explain how holding companies and subsidiaries work.

What Happens When The Subsidiary Company Is In Debt?

Even though a subsidiary company is technically separate from its parent company, liability can still extend to the holding company.

More specifically, the holding company can be liable for the debts of its subsidiaries where the subsidiary company is trading while insolvent and a director knew, or should have known, about it.

If you’re unsure about whether a holding company could be liable, you can ask the following questions:

- Was it a holding company of the subsidiary at the time that the debt was incurred?

- Was the subsidiary company insolvent at that time?

- Were there reasonable grounds for suspecting that the subsidiary company was insolvent, or would become insolvent?

- Were one or more directors aware (or should have been aware) that there were reasonable grounds for suspecting insolvency?

If any of these points apply to your situation, your holding company can be liable for your subsidiary company’s debts.

As a director of a holding company, it’s important to closely monitor the financial status of your subsidiary companies.

What Can A Liquidator Do?

If your subsidiary company is in debt, a liquidator will be appointed to manage their financial situation. Under section 588W of the Corporations Act, the subsidiary’s liquidator can recover the money from the holding company if:

- The holding company has breached s 588V (this section states that a holding company is liable if they knew, or should have known, about the subsidiary’s insolvency)

- The person that is owed money has suffered loss or damage due to this insolvency

- The debt was wholly or partly unsecured at the time of loss or damage

- The subsidiary company is being wound up

If the above applies, the liquidator can recover the owed money from the holding company.

What Defences Can I Use?

Setting up a holding company doesn’t exclude all risks of liability. Thankfully, there are some defences available should you ever find yourself in this kind of situation (these are set out in section 588X of the Corporations Act).

Safe Harbour Provisions

If your holding company is being held liable for the subsidiary company’s debts, you can claim that you were developing a plan that was ‘reasonably likely to lead to a better outcome’ for the company. This is known as a safe harbour provision.

These provisions are particularly helpful for businesses during the stressful COVID-19 situation as it allows directors to seek relief where insolvency is difficult to avoid. Essentially, it’s the director’s way of saying that while they knew of the insolvency, they were doing what they could to manage it.

Reasonable Grounds

As a holding company, you can claim that there were reasonable grounds to believe that the subsidiary company was actually solvent. This means you reasonably believed that they were able to pay all of their debts, and would continue to be solvent even when they did incur the debt.

Reliance On Information

The holding company can also claim that a ‘competent and reliable person’ was responsible for giving them enough information about whether the company was solvent, was giving them this information, and based on this information, they reasonably believed that the subsidiary company was solvent.

Director’s Non-Participation

A holding company can also use the defence that its directors were unable to assist in managing the company due to an illness or another good reason. Essentially, the company can claim that the director’s absence made it impossible to know of the insolvency.

Reasonable Steps Taken To Prevent Insolvent Trading

Lastly, a holding company can argue that they took reasonable steps to prevent the subsidiary company from incurring the debt or trading while insolvent. In this case, the holding company may be able to avoid liability.

While there are a number of defences available for a holding company in this situation, it’s generally good practice to avoid this liability from the outset. A great way to do this is to monitor your subsidiary company’s finances regularly and ensure that there are no grounds to suspect insolvency.

Next Steps

Setting up a holding company has its benefits, but it doesn’t necessarily rule out the possibility of liability for your subsidiary’s debts.

Luckily, we have a team of lawyers you can chat to about a Dual Company Structure and any concerns you have regarding liability.

Feel free to reach out to us at team@sprintlaw.com.au or contact us on 1800 730 617 for an obligation free chat.

Get in touch now!

We'll get back to you within 1 business day.

Top 3 Legal Mistakes

Top 3 Legal Mistakes

Book in a free consultation with us to discuss your legal needs.